Industrial 3D Printer Shipments Weather Chaotic Market

Vendors optimistic about 2025 recovery, analysts report.

Latest News

January 17, 2025

The third quarter of 2024 was challenging for the global 3D printing market, marked by weak financial results, layoffs, leadership changes, CEO turnover, operational scalebacks and contentious mergers and acquisitions. Industrial ($100,000+) and midrange ($20,000–$100,000) system shipments dropped by −24% and −8% year-over-year, respectively, according to global market intelligence firm CONTEXT.

“There were some rays of hope that shone through,” says Chris Connery, vice president of global analysis at CONTEXT. Sales in the Professional ($2,500–$20,000) price class were only marginally down on the previous year (−1%) and shipments of entry-level (under $2,500) printers continued to rise, increasing 28% year-on-year (YoY). “There was even success for some vendors in the struggling Industrial sector as Eplus3D and Nikon SLM Solutions both enjoyed success with their super-advanced, multi-laser, high build-volume metal powder bed fusion (PBF) machines.”

Click here for full-size Chart 1.

Industrial Systems

The quarterly −24% drop in Industrial system shipments pushed yearly shipment trends into the red, with shipments now down −19% for the trailing-twelve-months (TTM). The marked drop in the Industrial price class affected almost all printer modalities and material types. Globally across all regions, both Industrial metal and Industrial polymer shipments were down in the period by almost equal measure (-24% and -25% respectively).

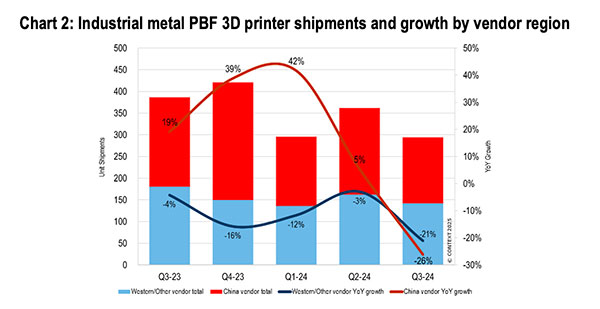

Industrial Metal Systems

Shipments of metals printers were holding up better than those of polymer systems until the second quarter of last year when both saw YoY falls. In Q3-24, binder jetting system sales were flat but shipments of printers using other technologies again declined. PBF systems accounted for 74% of new industrial metals systems in this period but shipments of these were down −24% on the previous year.

Midrange Systems

Reduced spending in the industrial price class continued to trickle down into the midrange market and contributed to an −8% YoY drop in shipments in Q3-24. Stratasys kept hold of its market share lead but saw weak sales of some lines, especially material extrusion printers. 3D Systems is getting smaller each quarter and dropped to sixth place in this price class as it continues to struggle.

Professional Systems

The bounce-back in the professional price class was driven almost completely by Formlabs. Although overall shipments for Q3-24 were still down −1% YoY, and −20% on a TTM basis, the rollout of Formlabs’ new LFD vat photopolymerization platform led to the shipment of 26% more vat photo printers than in the same period of 2023.

Entry-level Systems

Entry-level printer shipments were up 28% YoY in Q3-24 and a whopping 43% on a TTM basis. Growth slowed for Creality and, although it continued to lead the price class, there were market-share gains for companies such as upstart Bambu Lab and long-time player Flashforge.

Outlook

The 3D printing market saw a turbulent end to 2024. The top question surrounds the fates of Desktop Metal and Markforged as Nano Dimension has made wholesale changes to management and board that put its planned acquisition of these companies in doubt. Other vendors, including BigRep and Prodways, have also seen leadership changes, while long-term player voxeljet has announced plans to sell to a technology investment firm. Elsewhere, Nexa3D has significantly scaled back operations and Velo3D was seemingly recently saved from the brink of bankruptcy.

“While this chaos had significant impacts, newly updated analyses show that 2024 as a whole was even more heavily affected by high interest rates and subsequently muted CapEx spending,” says Connery. “It therefore seems that full-year figures are likely to be close to the lows seen during the height of pandemic lockdowns in 2020 with at least −12% fewer Industrial printers shipped worldwide in 2024 than in 2023.”

Looking further ahead, the current forecast for 2026 is of more consistent and stronger double-digit YoY growth in all sectors with YoY growth rates upwards of 30%−40% over a 5-year horizon.

“To put this in context, note that the market bounced back strongly coming out of Covid as vendors delivered against pent-up demand: between 2020 and 2021, Industrial 3D printer shipments were up 30% and those of Midrange systems increased by 26%,” says Connery. “However, the impact of a change in U.S. government is yet to be determined: while the new administration is generally focused on accelerating business potential, sticky inflation and unknown import restrictions are tempering optimism.”

* Price classes: Personal <$2,500; Professional $2,500–$20,000; Midrange $20,000–$100,000; Industrial $100,000+

Sources: Press materials received from the company and additional information gleaned from the company’s website.

Subscribe to our FREE magazine, FREE email newsletters or both!

Latest News

About the Author

DE’s editors contribute news and new product announcements to Digital Engineering.

Press releases may be sent to them via DE-Editors@digitaleng.news.